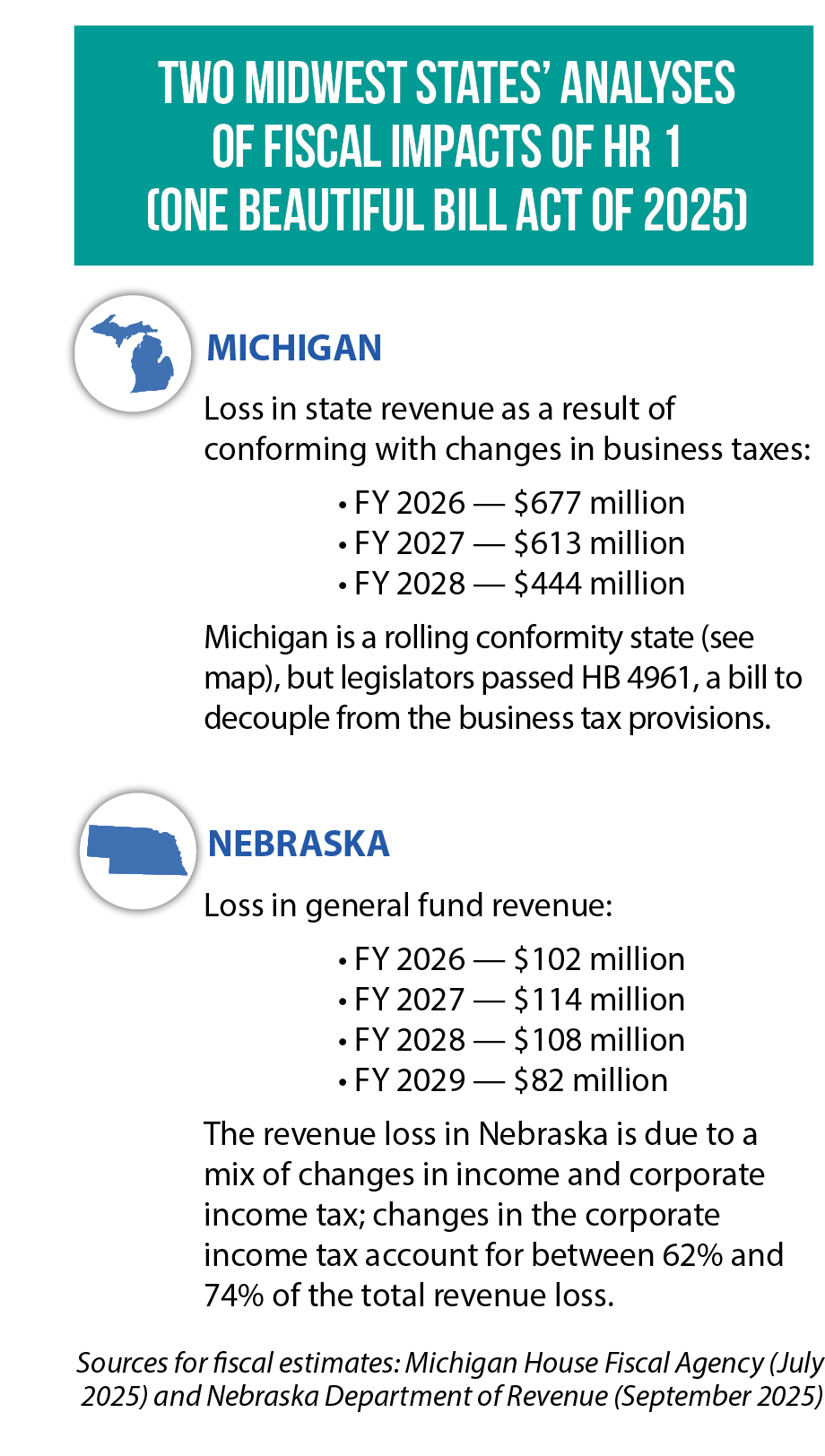

Not long after the U.S. Congress passed a sweeping new law with big changes to federal tax law, Michigan legislators found themselves debating it as part of their own budget negotiations. The question before them: When should our own state’s tax code conform with provisions in the One Big Beautiful Bill Act (HR 1 of 2025), and when should we decouple?

They ultimately decided on a mixed approach. As signed into law, HB 4961 conforms with some of the federal law’s most talked-about features, namely new tax benefits for workers who earn tips or overtime pay and for individuals who have Social Security income. In the same bill, though, legislators chose to decouple Michigan’s state tax code from multiple corporate income-tax provisions in HR 1 — for example, the federal law’s immediate deduction of research-and-development expenses and its 100 percent deduction for qualified production property.

They ultimately decided on a mixed approach. As signed into law, HB 4961 conforms with some of the federal law’s most talked-about features, namely new tax benefits for workers who earn tips or overtime pay and for individuals who have Social Security income. In the same bill, though, legislators chose to decouple Michigan’s state tax code from multiple corporate income-tax provisions in HR 1 — for example, the federal law’s immediate deduction of research-and-development expenses and its 100 percent deduction for qualified production property.

“As far as the coupling versus decoupling [on the corporate tax side], those were things initiated and effective in the middle of a tax year,” Michigan Rep. Ann Bollin says. “We felt by continuing the schedule as is, we’re not going to create any additional harm to businesses. So, they still get the federal benefit, but the state benefit stays on the same schedule.”

Across the country, state legislators are facing similar choices.

“Congress often tinkers with the tax code from one year to the next, so state conformity debates happen all the time, says Carl Davis, research director at the Institute on Taxation and Economic Policy. “But they’re usually much more minor considerations.”

‘Whole new level’ of debate

HR 1 is widely considered to have ushered in the largest changes in federal tax policy since at least the Tax Cuts and Jobs Act (TCJA) of 2017. The 2025 bill made a majority of the TCJA’s provisions permanent, while also adding new short- and long-term tax rules.

“These conformity debates, the high-profile conformity debates, are kind of like cicadas: They’ll come around once every several years and you can kind of see it coming,” Davis says. “Anytime you have a major federal tax rewrite that passes and changes the tax base in significant ways, these conformity debates are elevated to a whole other level. There’s a lot more revenue on the line.”

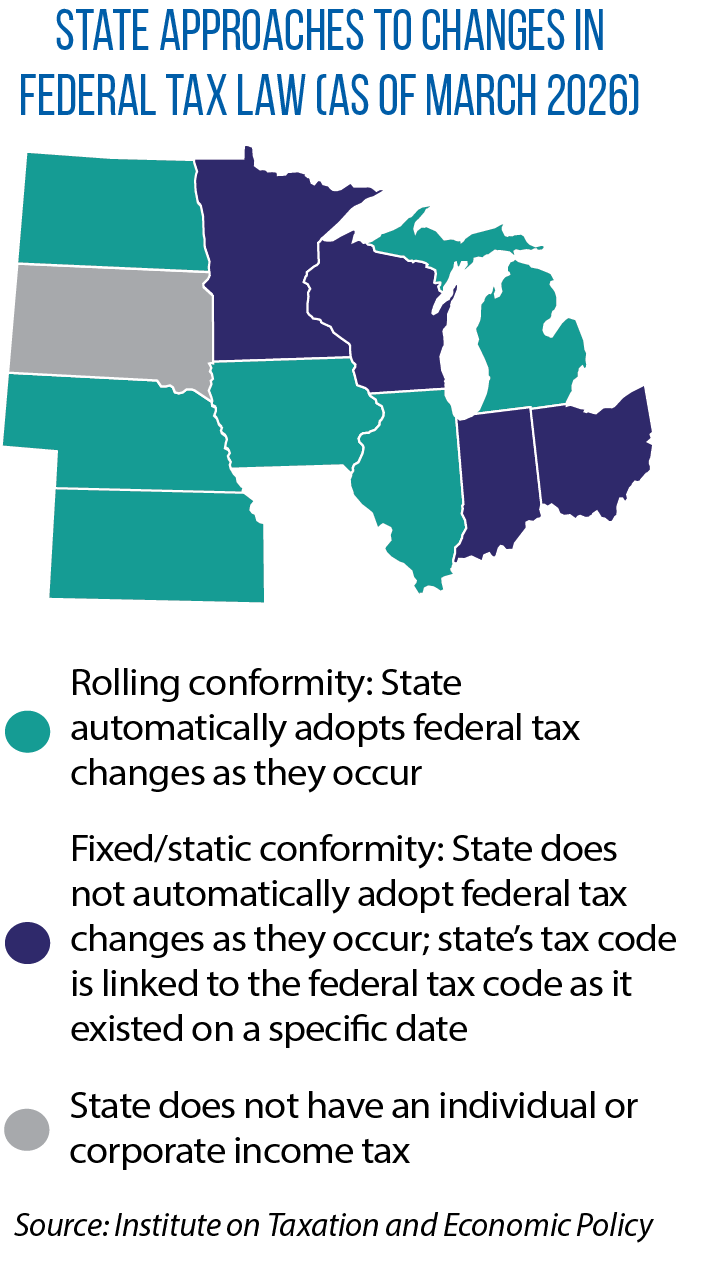

From state to state, laws vary on what type of legislative action is needed in response to changes in federal tax law. Michigan, for example, is typically categorized as a “rolling conformity” state, meaning it has statutory language to automatically adopt changes in federal tax law as they happen. To decouple, a bill must be passed by the Michigan Legislature and signed by the governor.

Rep. Ann Bollin

“It’s the responsibility of the Legislature … to always be looking at that,” Bollin says, noting the need to regularly review changes in the Internal Revenue Code and ensure they align with the state’s needs.

Along with Michigan, Illinois, Iowa, Kansas, Nebraska and North Dakota are rolling conformity states, according to the Institute on Taxation and Economic Policy. In contrast, Indiana, Ohio, Minnesota and Wisconsin adhere to “static conformity”: modifications to the state tax code are not automatically adjusted to conform with changes in the federal tax code. Minus legislative action, decoupling occurs because the conformity is “static,” set to the federal tax code as of a fixed or predetermined date.

Essentially, static conformity provides an opt-in approach for legislatures; rolling conformity an opt-out model. There are advantages to both, Davis says, though he prefers the former.

“State lawmakers should craft the tax code that makes sense for their state, and because of that, static conformity gives them a little more control,” he says. “You’re not running the risk of things just getting folded in without knowing about it or thinking about it or voting on it, just because Congress thought it was a good idea.”

There also can be a middle-ground approach.

Davis points to Maryland as an example. It is a rolling conformity state, but with this caveat: If a federal change would impact annual state tax revenues by $5 million or more, it triggers a temporary decoupling of state tax code for a single tax year. The intent of this statutory language is to give legislators time to either permanently decouple or conform.

In a January 2026 report, the Maryland comptroller alerted the General Assembly that three aspects of HR 1 would have an impact greater than $5 million for the 2025 tax year, thus triggering a temporary decoupling.

- Allow for immediate and full deductions of domestic research-and-development expenses;

- Reverse TCJA interest deduction limitations; and

- Provide a temporary 100 percent deduction for investment in “qualified production properties,” including certain manufacturing, production and refining facilities.

State responses to HR 1

Conforming to the federal tax code provides advantages to states, including greater administrative simplicity and reduced chances of double taxation. There also can be a benefit to relying on federal court precedents to interpret tax laws.

Not all federal tax provisions are beneficial for individual states, however, and legislatures have the option to choose the provisions they wish to opt out of or decouple from. In fact, no state conforms completely to the Internal Revenue Code, each modifying it in various ways.

Not all federal tax provisions are beneficial for individual states, however, and legislatures have the option to choose the provisions they wish to opt out of or decouple from. In fact, no state conforms completely to the Internal Revenue Code, each modifying it in various ways.

In response to HR 1, rather than relying on automatic opt-ins or opt-outs in statute, many state legislatures have taken action to accept or decouple from the changes in federal law. Michigan’s HB 4961, signed into law in fall 2025, is one example of a state response in the Midwest to HR 1.

Additionally, Illinois (like Michigan, a rolling conformity state) decoupled from parts of HR 1 with the passage of SB 1911. The bill decoupled the state from the 100 percent deduction for qualified production property while conforming to changes in the definition of taxable corporate foreign income.

Indiana (SB 212) and Ohio (SB 9) explicitly updated their base conformity to the most recent tax year, adopting aspects of HR 1. This year’s omnibus tax bill in Minnesota (HF 2438, signed into law in May) includes several provisions to conform with the federal tax code.

States also have the option to change their approach to conformity altogether.

Nebraska’s LB 857, introduced in early 2026, would shift the state from rolling to static conformity. A note prepared by state fiscal analysts estimates that the change would result in a net revenue gain of $103 million in fiscal year 2027. LB 857 did not advance prior to the close of session.

|

Tax Conformity Laws Enacted Since Congressional Passage of HR 1 of 2025: Examples from the Midwest

|

||

|

State

|

Bill(s)

|

Summary

|

|

Illinois

|

Conforms to federal:

• Transition from Global Intangible Low-Taxed Income (GILTI) to Net Controlled Foreign Corporation Tested Income (NCTI). Illinois allows for a 50% deduction for NCTI. Decouples from federal: • IRC §168(n): 100% deduction for qualified production property • IRC §168(K): 100% bonus depreciation |

|

|

Indiana

|

Conforms to federal:

• Internal Revenue Code (IRC) as of January 1, 2026 Decouples from federal: • IRC §168(n): 100% deduction for qualified production property • IRC §168(K): 100% bonus depreciation • IRC §174A: Immediate deduction of domestic R&D expenses • IRC §163(j): Business interest expense limitation (remains decoupled) |

|

|

Michigan

|

Conforms to federal:

• IRC as of January 1, 2025 Decouples from federal: • IRC §168(n): 100% deduction for qualified production property •IRC §168(K): 100% bonus depreciation • IRC §174A: Immediate deduction of domestic R&D expenses • IRC §179: Expensing for small business property • IRC §163(j): Business interest expense limitation |

|

|

Minnesota

|

Conforms to federal:

• IRC as of May 1, 2026 Decouples from federal: • IRC §174A: Immediate deduction of domestic R&D expenses • IRC Section 1400Z-2(a): Opportunity Zones permanent extension • IRC §21: Child and dependent care credit • Definition of NCTI; adopted its own |

|

|

Ohio

|

Conforms to federal:

• IRC as of March 5, 2026 Decouples from federal: • IRC §168(K): 100% bonus depreciation • Certain Section §179 deduction limits |

|

The post Conform or decouple? Changes in federal tax policy stir debates in state legislatures appeared first on CSG Midwest.