Please note that this article is based on projected results and may change with certified election results.

Polls are closed on the 2022 general election where voters in 46 states decided on 6,278 state legislative races, 36 governors and 133 statewide ballot measures. The Council of State Governments, the nation’s only nonpartisan organization serving all three branches of state government, will provide coverage and analysis of state elections with attention to state races and the impact of ballot measures. This article provides an overview of the results and trends in state races and ballot measure results based on projections made through midday Nov. 9.

States are seeing increased diversity in elected candidates.

Several races, projected by Ballotpedia, are historical firsts, expanding gender, race and age representation amongst elected officials. Governor Sarah Huckabee Sanders (R), former press secretary for President Donald Trump, made history in Arkansas as the first female governor in Arkansas. Governor Maura Healy (D) of Massachusetts and Governor Kathy Hochul (D) of New York also made history as the first female elected governor in their respective states. Governor Healy is also the first openly lesbian governor in the US and the first openly gay governor in Massachusetts. U.S. Representative Marcy Kaptur (D) became the longest-serving female member of Congress with reelection to Ohio’s 9th District. Governor Wes Moore became the first Black governor of Maryland and his lieutenant governor, Aruna Miller (D), is the first immigrant and first Asian American to be elected to statewide office in Maryland. In Rhode Island, Chinese American Victoria Gu (D) and Japanese American Linda Ujifusa (D) became the first Asian candidates elected to the state legislature, and Shri Thanedar (D) became the first Indian American U.S. Representative for Michigan. Maxwell Frost (D) won Florida’s 10th Congressional District race, making him the first Democratic member of Congress from Gen Z and the first Afro-Cubano to head to Congress.

Partisan legislative and state control remains steady with Democrats consolidating power in some states.

So far, Democrats have consolidated power in several states – Maryland, Massachusetts, Michigan and Minnesota. Previously, these states were under a divided government. No new state government trifectas have been called for Republicans yet, and no state governments that were trifectas controlled by one party have moved to divided government yet. However, these results may change as more state elections are called. Partisan legislative control remains relatively steady as election results are projected. The Democratic Party in Minnesota has consolidated legislative power from previously split control, and Michigan has flipped from Republican legislative control to Democratic control. Results have not yet been projected for six states which may change these results.

Incumbent Governors are being re-elected and the Democratic party has gained some control.

This year there are 36 governor seats up for reelection, currently, 32 of the races have been called. Seven governors did not seek reelection. Democrats have picked up two governor seats in Maryland and Massachusetts. Currently, every incumbent governor that was up for reelection has won. There are currently six newly elected governors; Maura Healy (D) Massachusetts, Sarah Huckabee Sanders (R) Arkansas, Jim Pillen (R) Nebraska, Josh Green (D) Hawaii, Josh Shapiro (D) Pennsylvania and Wes Moore (D) Maryland. Governor races that have not been confirmed yet are Alaska, Arizona, Nevada and Oregon. In the US Territories incumbent Lou Leon Guerrero (D) won reelection in Guam. Incumbent Albert Bryan (D) won reelection as governor of the US Virgin Islands while incumbent Ralph Torres (R) is facing a runoff versus Arnold I. Palacios (I).

With his win in Maryland, Wes Moore is a growing figure nationally among Democrats. Governor Ron DeSantis handedly won reelection in Florida by wide margins and continues his growth as a leader in the GOP and potential presidential candidate in 2024.

States have passed ballot measures addressing state legislative authority, election administration and voting-related policies and state tax changes.

On the ballot this year were several possible changes to some states’ constitutional amendment processes. So far, Arizona’s Proposition 132 is too close to call. If enacted, this measure will require a 60% majority for future constitutional amendments that approve new taxes. In Arkansas, Issue 2 was defeated. This measure would have required a 60% majority for future constitutional amendments.

Some states considered changes to voting policy and election administration. Nebraska voters approved Initiative 434, requiring a photo ID for voting. Ohio passed Issue 2, prohibiting local governments from allowing anyone who does not meet the qualifications for an elector (e.g. a non-citizen) to vote in local elections. Connecticut voters approved Question 1, allowing the legislature to establish early voting. Michigan approved Proposal 2, which made several changes to voting procedures including creating a 9 day early voting period, requiring photo ID, requiring military and overseas ballots postmarked by election day to be counted, prohibiting voter intimidation and several other changes. A proposed photo ID requirement in Arizona and Nevada’s possible adoption of ranked choice voting are still too close to call.

At least six states proposed ballot measures changing state tax laws. In California, voters rejected Proposition 30, which would have raised taxes on those making more than $2 million to subsidize electric vehicle infrastructure and wildfire prevention. Colorado voters passed Proposition 121, lowering the income tax from 4.55% to 4.40%. West Virginia failed to pass Amendment 2, which would have allowed lawmakers to exempt property taxes on motor vehicles and personal property used by businesses. The results of Arizona’s Propositions 130 and 310, allowing lawmakers to pass a personal tax exemption and increasing sales taxes to fund fire districts, are too early to call. Massachusetts voters passed Question 1, imposing an additional 4% tax on those making over $1 million to fund education and transportation. Idaho approved the Advisory Question, which asked voters for their opinion on tax changes including additional rebates to taxpayers, reduction of the corporate tax rate and allocation of tax revenue to education.

States have passed ballot measures addressing the regulation of marijuana, abortion and enslavement.

Several state elections included ballot measures addressing marijuana, abortion and enslavement. According to the Pew Research Center, Millennials are at the forefront of the recent rise in public support for the legalization of marijuana and abortions. It is likely that these ballot measures motivated Millennials and younger generations to vote in the 2022 elections.

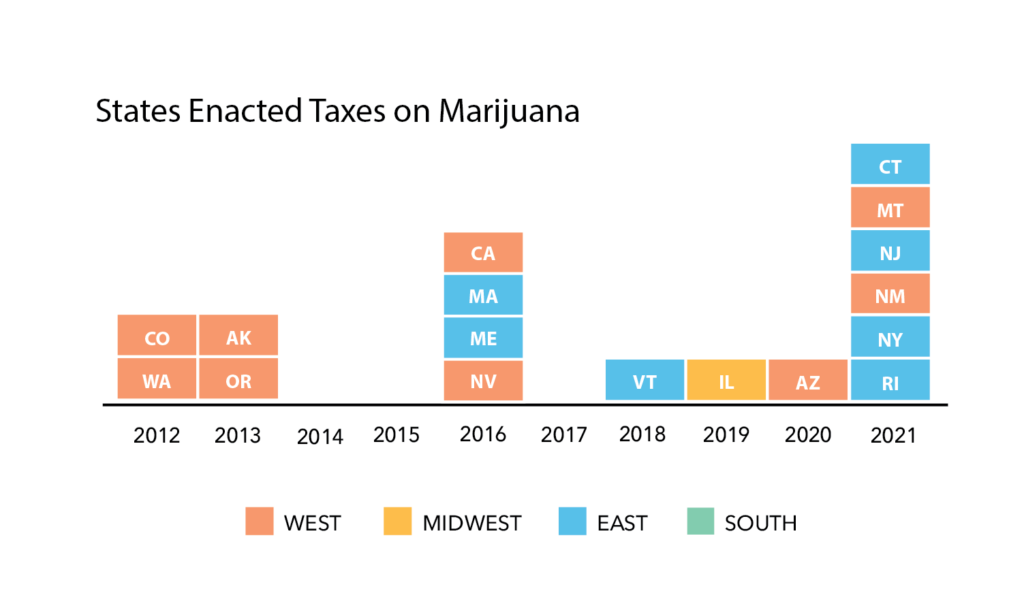

Before the elections, marijuana was legal in 19 states and D.C. Of those 19 states, 13 and D.C. had legalized marijuana through the ballot measure process. During the 2022 midterm elections, Maryland and Missouri passed ballot measures legalizing marijuana. Arkansas, North Dakota and South Dakota rejected ballot measures legalizing marijuana.

There were five ballot measures addressing abortion in the midterm elections. California, Michigan and Vermont voted to add “reproductive freedom” to their state constitutions, and Kentucky voted no to a constitutional amendment stating nothing in the state constitution creates a right to abortion or requires government funding for abortion. Montana results are not confirmed, but current results look like abortion rights will remain.

As of October 2022, 20 state constitutions included language permitting enslavement or servitude as criminal punishment or debt payments. During the 2-22 midterm elections, five states had ballot measures repealing such language. Alabama, Oregon, Tennessee and Vermont have voted to repeal language allowing slavery or involuntary servitude as criminal punishments. Louisiana voted not to repeal language allowing involuntary servitude as criminal punishments which may be due to confusion with the wording of the ballot measure.

CSG will continue to provide initial results on key topics as well as more in-depth analysis in the days following the election. Find those articles on Twitter (@CSGovts) and at csg.org/state-talk.